For rational investors, at the current valuation, Tesla Motors (TSLA US) presents an unparalleled chance to buy a large capitalisation growth stock with an addressable market of hundreds of billions of dollars. Tesla will likely capture a significant share of the transportation industry profit pool going forward. While traditional automakers play the BCG matrix to reposition the product portfolio, Tesla offers a pure, unencumbered play on green energy, electric vehicles and China: all rolled into one.

Elon Musk (“Musk”), the chief evangelist for Tesla Motors (TSLA US) ( “Tesla” or the “Company”) took one puff of marijuana on youtube, and all hell broke loose. For the uninitiated, marijuana use is legal in California and many other U.S. States, although federally in the U.S., it is still a controlled substance. Marijuana is already legal in Canada for medicinal purposes, and will also become legal for recreational use beginning October 17, 2018. It is interesting indeed that all this furor surrounding Musk’s usage of a substance on the verge of being widely accepted is similar to electric cars becoming widely accessible and adequate as a mode of transportation. Not to suggest that the high of the Ludicrous mode in a Tesla X P100D is the same as the high attained by Bob Marley while recording Kaya!

Nonetheless, placing the infamous inhaling of Kaya, alongside the now very public failure of a going private transaction at a suggested stock price of $420/share (wink-wink nod-nod), gives credence to bearish folklore of an unhinged CEO, and allows haters to continue to pound the table on the coming demise of Tesla. So what’s a rational investor to do? In ANTYA’s view, Investors with the fortitude to withstand the gut-wrenching volatility of owning a stock with the possibility of changing the career trajectory forever, i.e. hero to zero or vice-versa, need to look beyond the glaring and misplaced media headlines and hunker down.

We have been bearish on many media darlings in the past, and in every instance, the company imploded within two or three years, because of one of the following reasons outlined below, or in some unfortunate instances multiple reasons coming together at the same time. This is the first time we are in the midst of a battle where a majority are bearish, while we retain our bullish stance. It will be interesting to see who ends on the tombstone on this one. Coming back to fallen angels of yore:

- Related party dealings are hidden from public view, e.g. Valeant Pharmaceuticals Inc.

- Aggressive accounting is masking M&A-driven growth masquerading as organic performance, i.e. unreliable financial statements, e.g. Yellow Pages Income Fund, Valeant Pharmaceuticals Inc.

- Hiding the secular downturn in business using aggressive accounting, e.g. Nortel Networks Inc. and Yellow Pages Income Fund

- Using unproven technology to de-risk business,e. g. MDS Inc.

We could list 100 other instances, but discourse is not what investors require of us. Investors in Tesla will agree with the following facts:

- The Electric Vehicle industry is at the very beginning of the adoption of S-Curve and has not yet started climbing up on it.

- Tesla’s technology and products are far superior to those of existing competitors (we do not believe there are any yet, but for those automakers that will one day launch real products) and have a proven track record globally in a variety of climatic and road conditions.

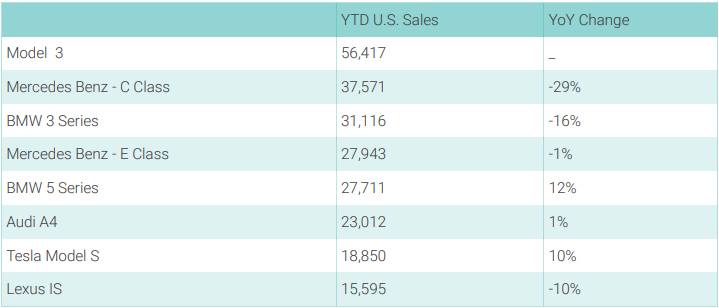

- Tesla’s Model S and Model X production capabilities are proven, whereas Model 3 is beginning to gain traction. YTD data as highlighted in Figure 1 is illustrative of Tesla’s success in the U.S. and worldwide, and proves that Tesla is a formidable foe of traditional automakers; especially the premium cars.

Source: ANTYA Investments Inc. and goodcarbadcar.net

- Many observers of the automotive industry including Henry Kwon have voiced concerns regarding the need to update Model S, given that it is entering its 6th year without a major upgrade. If those concerns are correct, then Tesla is not feeling the pinch yet because YTD sales in the U.S. are up 10%. Moreover, with a slowdown in Tesla sales in China, as discussed in TSLA Exports to China Collapsed Post Auto Import Tariff Hike, it is plausible that Tesla could pull back inventory scheduled for China and sell more in the U.S. resulting in additional gains, though at lower profitability perhaps.

Therefore, in ANTYA’s opinion, rumors suggesting a Tesla debt default, or the Company’s demise are greatly exaggerated. By the time so-called “Tesla Killers” – funny nomenclature –, as discussed in Tesla (TSLA): The Impending Onslaught of Tesla Killers from Porsche, Audi and Mercedes arrive in reality and at scale, Tesla’s China Gigafactory in Shanghai and another factory in Europe – most likely in Germany – would be up and running. In our estimate, Tesla would be close to producing a million vehicles per year by 2022, with approximately 500,000 in 2019.

A Quantitative Perspective

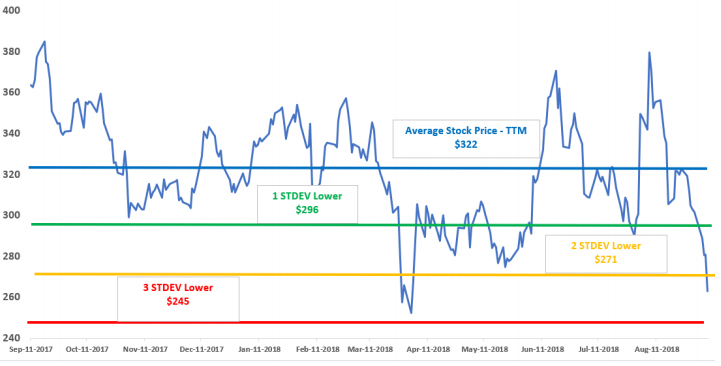

Figure 2 presents Tesla’s stock trajectory on a trailing twelve months basis and highlights some crucial quantitative measures.

Source: ANTYA Investments Inc. and Capital IQ

If you have read so far, it is apparent that we are not bearish on Tesla, notwithstanding the excruciating pain of holding the stock and riding a roller-coaster. Figure 2 outlines the stock price trajectory for the trailing twelve months ended September 07, 2018 (“TTM”). The average stock price shown in blue has been $322/share, with the standard deviation – calculated on a daily basis – at $26/share. At its Friday close of $263/share, Tesla is trading at 2.26 standard deviations below its average for TTM.

That results in a forward EV/EBITDA multiple of less than 18x 2019 consensus EBITDA estimate of $3.4 billion and a ridiculously low multiple of 11.1x 2020 consensus EBITDA of $5.1 billion. ANTYA believes that both EBITDA estimates will be revised upwards by street analysts after Q3-18 results. The last time Tesla traded at a below 18x multiple around the time of

unsubstantiated reports of an autonomous car accident, the stock rebounded sharply. The probability of further declines is minuscule, while that of regaining ground to $322, with 22% upside from current levels is significant.

The whole thing about Tesla’s chief accounting officer leaving after one month is a red-herring that needs to be overlooked. Tesla executive departures as discussed in the following story from Reuters Factbox: Tesla executive departures since 2016, is far from a revolving door of talent exit. It speaks to a dynamic job market in the valley where Tesla talent is in demand.

For rational investors, at the current valuation, Tesla presents an unparalleled chance to buy a large capitalization growth stock with an addressable market of hundreds of billions of dollars, with an opportunity to capture a significant portion of the industry profit pool. While traditional automakers play the BCG matrix to reposition the product portfolio, Tesla offers a pure, unencumbered play on green energy, electric vehicles, and China: all rolled into one.