Billion-dollar deals fall from the blue skies of China daily. Billion RMB even more so. Tencent Music Entertainment’s (TME US) agreement to buy Ultimate Music Inc. is a head scratcher that investors need to get a handle on. Yes, it is a Pre-IPO deal, but the same management will be responsible for post-IPO prospecting as well. Happy investing ?

Following up on our previous insight on Tencent Music Entertainment Group (“TME” of the “Company”) in this update we look at the acquisition of Ultimate Music Inc. (“Ultimate) by TME in 2017. Although the experience has shown that billion-dollar deals just fall from the blue skies of China, the acquisition of Ultimate by TME still appeared interesting enough that we decided to apprise prospective investors about it as well. Although TME is a private company, it is majority-owned by Tencent Holdings (700 HK) which is publicly traded in Hong Kong and in the U.S. as well. It is not clear if external stockholders such as Spotify Technology Sa (SPOT US) which owns approximately 9% of TME have any sway over deal-making at TME.

The story goes thus. Ultimate, acquired by TME in 2017, was established by Tsai Chun Pan, Group Vice President of Ultimate Music, in 2014. Mr. Pan’s credentials are exemplary with a bachelor’s degree in Japanese studies from SOAS, University of London, and a master’s degree in marketing management from Cranfield University. Mr. Pan is working closely with various smart device and automobile manufacturers to assist them in developing built-in music players into their respective systems.

TME acquired 100% equity interest in Ultimate in October 2017 and promptly disclosed a step-up gain upon fair valuing the equity interest held at the time of the deal. TME said in its prospectus that:

Our other gains, net, was RMB124 million (US$19 million) in 2017, as compared to other losses, net of RMB13 million in 2016. The change was mainly due to (i) a gain on the step-up acquisition of Ultimate Music in the amount of RMB72 million (US$11 million), (ii) increased government grants, and (iii) net foreign exchange gains.

TME thus took control of a company it already owned partially, though how much was not evident to us.

How much did TME Pay to buy Ultimate?

As per the disclosure of TME, the purchase consideration for Ultimate comprises of:

- An aggregate amount of approximately RMB463 million to be settled unconditionally, including cash and certain ordinary shares of the Company to be issued before June 30, 2018 (“Unconditional Consideration”)

- cash of US$26 million to be paid in certain installments in 4 years;

- approximately 26,543,339 or ordinary shares of the Company to be issued in several tranches in the coming years, subject to certain conditions; and

- issuance of 2,743,860 ordinary shares to [certain] entities in consideration for their performance of certain license contracts with Ultimate

ANTYA estimates that TME is expending approximately RMB1.42 billion on Ultimate based on TME’s pre-IPO valuation. According to TME;

As a result of the acquisition, the Group is expected to increase its presence in online music industry in China.

That’s all well and good, but it is unclear to us as to how a nascent venture which currently appears to be at worst an idea and at best a work in progress, fulfills TME’s stated intent of increasing its presence in China’s online music industry. Moreover, ignoring the future expenses associated with stock payments and cash payments, as illustrated in the purchase price allocation below, the entire purchase was accounted for as goodwill, which is neither deductible for tax purposes nor amortizable. Goodwill must be tested for impairment annually, and in our view, that should come soon enough.

TME explains that;

Goodwill arising from the acquisition was attributable to expected operating synergies as well as increase the coverage in the online music market in China. The goodwill recognized was not expected to be deductible for income tax purpose.

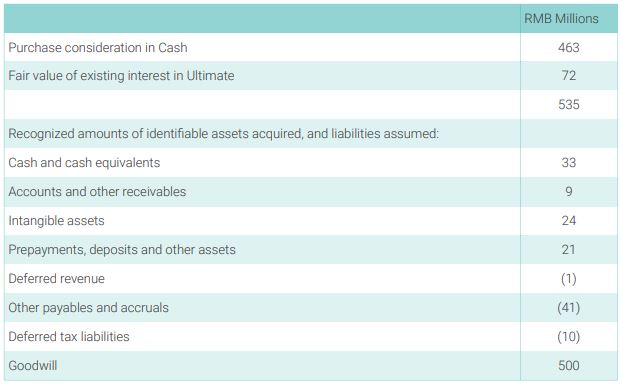

Figure 1 summarizes the consideration transferred by TME, and the amount of identified assets acquired, and liabilities assumed at the acquisition date.

Figure 1: What did TME Buy?

Source: Prospectus and ANTYA Investments Inc.

As highlighted in Figure 1, with only RMB1 million of deferred revenue on books (presumably for music subscription services since Ultimate is purported to be an online music business), TME has paid up for either management talent or something else which investors have no clarity on. Although given that these deals are Pre-IPO for incoming investors, the only lesson to draw is one on governance going forward. Are the check and balances and governance structures implied in the prospectus robust enough that going forward, investors will get better and more detailed information on management’s actions?

In the first half of 2018, employee compensation expense rose significantly with management attributing it to Ultimate. TME said that;

Our general and administrative expenses increased by 32.7% from RMB682 million for the six months ended June 30, 2017 to RMB905 million (US$137 million) for the six months ended June 30, 2018, which was mainly attributable to (i) an increase in our employee benefit expenses in connection with our acquisition of Ultimate Music in 2017 ….

Given that TME promised stock and cash payments to selling shareholders of Ultimate as discussed earlier, it is no surprise that G&A expenses shot up. What is surprising though is that only one of those employees/shareholders is a named officer, and the rest appear invisible to shareholders but valuable enough to cost more than RMB1.4 billion.

Should Incoming Shareholders Care?

That depends on what one makes of the following gem from acquisition-related disclosure.

The revenue and the results contributed by Ultimate to the Group for the period since the completion date were insignificant. The Group’s revenue and results for the year would not be materially different should the acquisition of Ultimate otherwise occur on January 1, 2017.

So TME is buying a business with a substantial capital outlay, which it acknowledges has little to no revenue, and its entire payment is unconditional. Why?

That is interesting indeed. TME acknowledges that Ultimate is essentially a development stage enterprise. However, TME is sassy enough to suggest to readers of its prospectus that RMB1.42 billion or thereabouts is a fair price for Ultimate because it will cement TME’s presence in the online music industry in China.

Happy Investing?