Although Nxp Semiconductors Nv (NXPI US) was left at the altar by Qualcomm Inc (QCOM US), the jilted bride has enough oomph left to attract other suitors, especially long-term value-oriented investors. We believe that at current levels the stock is undervalued and expect a 15% upward move within the next twelve months.

NXP Semiconductor N.V. (“NXPI”, or the “Company”) held its investor day on September 11, 2018, after a hiatus of two years. In the intervening period the entertaining saga involving Qualcomm, Broadcom Limited (AVGO US) and Elliott Advisors played out without providing an ending that pleased anyone. As discussed in our report NXP Semiconductors NV: Ignore the Noise, Go for It – Only Two More Days Left, we were mistaken in our view that the Chinese regulators would allow the deal to go through after approval had been obtained in eight other global jurisdictions including the U.S.

Nonetheless, we opined correctly that in the absence of a deal the downside was limited given the significant discount that NXPI was trading at compared to the offered price of $127 and that on a probability adjusted basis the investment was a good bet. On July 26, 2018, when the failure of the deal became public, the stock subsequently fell to approximately $93 from $98 the previous day and has remained around that level ever since, barring a precipitous fall during the investor day presentation. That brings us to the investor day.

We are encouraged by the Company’s many disclosures including:

- The initiation of a $1/share annual dividend implying a payout of approximately $300 million annually,

- Approximate 80% completion of the share-buyback announced after the failed Qualcomm deal. At the time the Company had said it would buy-back shares worth $5 billion in total,

- Significant reduction in financial leverage of the Company since 2015, with the ratio declining from 3.9x to 1.0x for 2017 and lower currently, thanks to the $2 billion bounties from Qualcomm; and

- The Company’s market and product leadership in the automotive sector provides headroom for growing cash flow and financial flexibility.

This is also an opportune time to discuss the recently announced acquisition of Integrated Device Technology by Renesas of Japan in a deal that ascribes an enterprise value of $6.7 billion to IDT. More details on the transaction and some of the reasons underpinning the agreement are discussed in the press release issued by Renesas available here Renesas to Acquire Integrated Device Technology, to Enhance Global Leadership in Embedded Solutions.

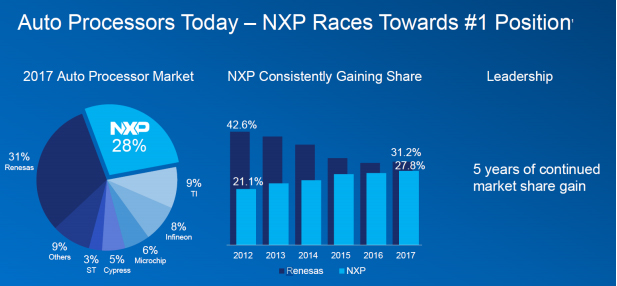

We bring up Renesas because at its investor day NXP highlighted Renesas as one of its main competitors in the auto processor market and disclosed that the Company has been gaining share as highlighted in Figure 1.

Figure 1: Auto Processor Competitive Landscape

Source: ANTYA Investments Inc. and NXPI

As highlighted in Figure 1, NXPI has been successful in challenging the hold of Renesas in the automotive market and has been gaining ground as the leader in the space. We provide the following quote Renases from its acquisition release to suggest that the actions of NXPI’s competitors corroborate the Company’s bullish view on the auto sector; “IDT’s analog mixed-signal products for data sensing, storage and interconnect are key devices that support the growth of data economy. Acquisition of these products enables Renesas to extend its reach to fast-growing data economy-related applications including data center and communication infrastructure, and to strengthen its presence in the industrial and automotive segments.”

Secular Growth in Advanced Autonomy and Electrical Vehicles

NXPI laid out a strong case for growing revenue by capitalising on the autonomy and increasing semiconductor content in cars. Given the changing worldview of manufacturers, customers, and fleet owners, NXPI’s worldview is defensible.

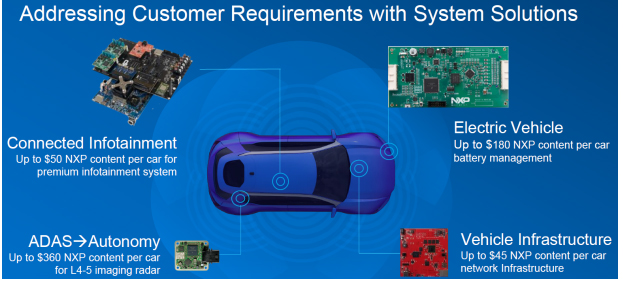

Figure 2 illustrates the revenue potential per vehicle for various products.

Source: ANTYA Investments Inc. and NXPI

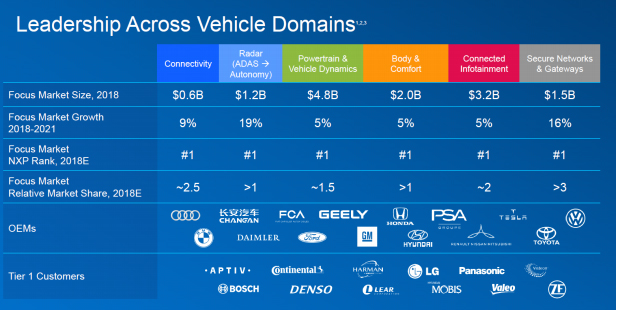

Given the changing dynamics of the automotive market, the contributions of different components to market growth overall and NXPI’s share is illustrated in Figure 3.

Figure 3: NXPI Leads the Market

Source: ANTYA Investments Inc. and NXPI

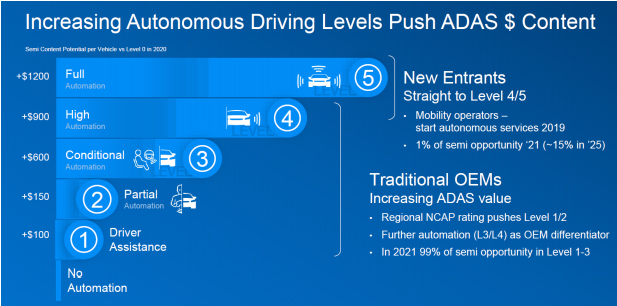

The Company is really focused on driving the Radar segment of the autonomy market where it is already the leader and is looking to maintain its premier status by partnering with other leaders on the computing side

while sharing its safety expertise with them. Figure 4 demonstrates the Company’s revenue expectation given the autonomous driving emphasis of all OEMs and new entrants into the industry.

Figure 4: The higher the autonomy, the more the revenue opportunity

Source: ANTYA Investments Inc. and NXPI

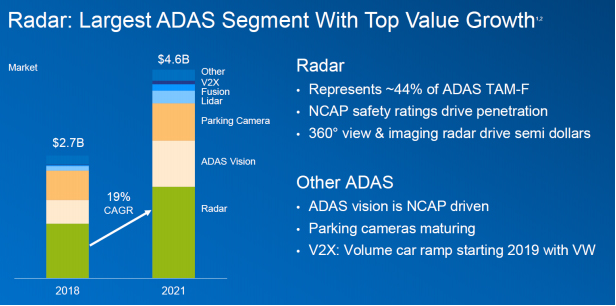

With NXPI banking on vehicle autonomy to grow its automotive operations , its market leadership in radar will play a critical role in delivering its financial objectives outlined for investors. Figure 5 presents that various components of autonomy and the addressable market for those components in 2021.

Figure 5: NXPI will fly in full view of the Radar

Source: ANTYA Investments Inc. and NXPI

NXPI has seen tremendous success in its product offering with 50+ vehicle platforms expected to adopt the company’s 77GHz solution for Level 3 autonomy over the next three years as disclosed in Figure 6.

Figure 6: Radar Shows the Way

Source: ANTYA Investments Inc. and NXPI

Given the backdrop of secular growth of the increasing use of semiconductors and modular systems to make autonomous driving a reality, and to enable the growing number of electric vehicles in their battery management operations, accompanied with NXPI’s leading market position, we believe that the financial targets outlined by the Company are attainable.

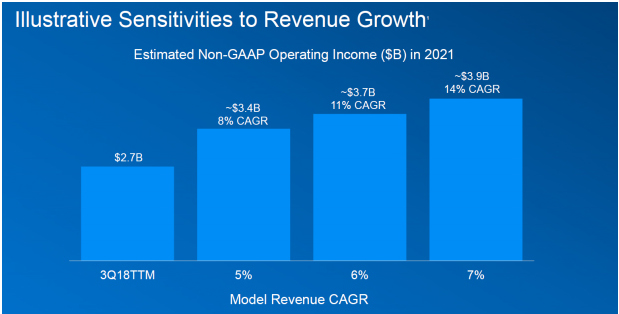

Figure 7 highlights management’s financial expectations based on our discussion so far.

Figure 7: EBITDA Growth in Various Scenarios

Source: ANTYA Investments Inc. and NXPI

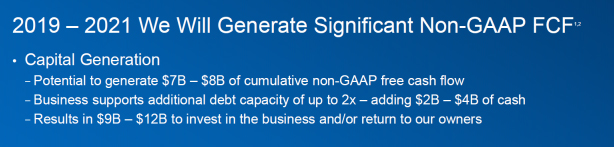

At the mid-point of management’s estimate of revenue growth, NXPI will deliver cumulative EBITDA growth of one billion dollars to 2021 from the current level of $2.7 billion, for the trailing twelve months. That implies good EBITDA growth of annualized 11%. More importantly, given limited capital expenditure requirements, NXPI will be generating substantial free cash flow as shown in Figure 8.

Figure 8: Robust Cash Flow Generation

Source: ANTYA Investments Inc. and NXPI

In ANTYA’s view, with approximately $12 billion of surplus cash flexibility over the next three years – $1 billion of which would go towards the newly introduced dividend- on the current enterprise value of $30.5 billion (CapitalIQ) investors cannot go wrong investing in NXPI. 25% of NXPI’s current enterprise value will come back to investors in the form of free cash flow to equity within three years.

Going back to Renesas bid for IDT, the valuation embedded within that bid is 20.5x, 2019 consensus EBITDA of 313 million.

Qualcomm’s increased bid for NXPI of $127.50/share was at a 2018 EBITDA multiple of 14.2x.

NXPI currently trades at 10.3x 2019 consensus EBITDA estimate of $2.93 billion.

Therefore, in our books, NXPI is undervalued.