Meituan Dianping (MEITUAN CH) is coming to the market at a difficult time. A slowing Chinese economy, a weaker currency and the threat of an all-out trade war could dampen investor sentiment. In ANTYA’s view, US$ 6.25/ share, or thereabouts, is a fair price for IPO investors to pay. That level provides a margin of safety and includes room for capital appreciation

Meituan Dianping (“MD” or the “Company”) is undertaking an IPO at a very precarious time in global trade and capital flows. President Trump’s “America First” agenda could be a red herring or result in a real policy shift. It is hard to tell! So far investors seem to believe in the former and not the latter, because global stock markets are volatile but flat. In ANTYA’s view, emerging market correction is driven more by the strength of the U.S. economy and the tightening monetary policy adopted by the Fed, causing currency depreciations vis-à-vis the USD – and now increasingly to be followed by the ECB and the BOE – rather than significant capital outflows from the EM asset class. May Unemployment Report–ANTYA Maintains View–Negative for EM Currencies, Bonds and The Japanese Yen provides our view on the EM asset class.

Mainland China IPOs of questionable or respectable companies such as Xiaomi Corp (1810 HK), Pinduoduo (PDD US), Qudian Inc (QD US) etc. have been fully subscribed whether in Hong Kong or on the NASDAQ suggesting continued and strong investor interest.

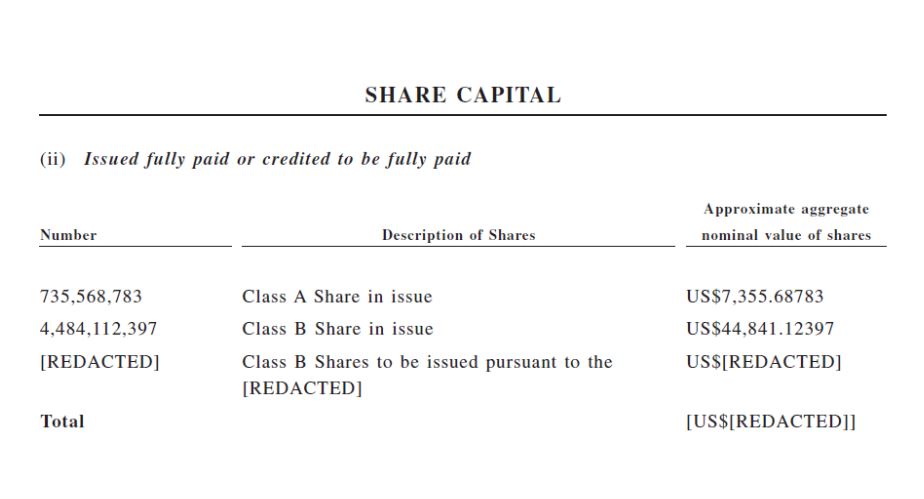

We have previously provided our views on Xiaomi Corporation (“Xiaomi”) in various reports including Xiaomi Inc. – Where Is the Transparency? Updated Equity Value Estimate of US$1/Share . While analysing Xiaomi, it was never clear to us as to how many shares in total would be outstanding after the IPO. The PR machine behind Xiaomi managed to obfuscate critical details from independent analysts (we assume SELL side knew better but maybe NOT!) and outside observers till the last moment. However, MD has provided much more succinct and lucid disclosure regarding shares outstanding prior to the shares expected to be allotted to outside investors as part of the IPO. Figure 1 highlights the details.

Figure 1: There is No Ambiguity in Share Count

Source: IPO Prospectus & ANTYA Investments Inc.

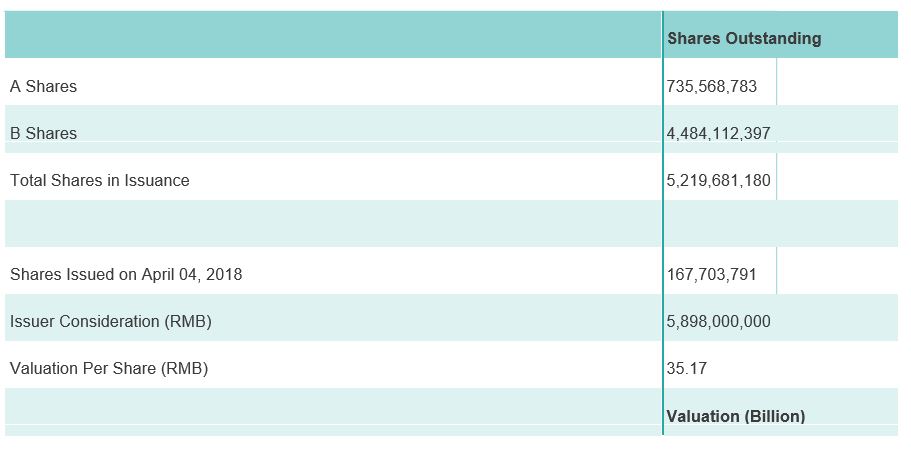

As illustrated, 735.56 million class A and 4.484 billion class B shares of MD are outstanding. MD also outlines in its prospectus that;

On April 4,2018, the Company issued an aggregate of 167,703,791 Series A-12 Preferred Shares ….”

Note 2 disclosed as a part of the Pro-Forma Net Tangible Asset Schedule informs us that;

Series A preferred shares issued subsequent to 31 December 2017″

based on the issuance consideration of RMB 5,898 million.

Therefore Most Recent Funding Round Valued MD’s equity at $27.82 Billion

Figure 2 presents the private market valuation of MD based on the funding round completed in April 2018.

Source: Prospectus and ANTYA Investments Inc.

Tencent Holdings (700 HK) and Qualcomm Inc (QCOM US) are amongst some of the major investors from the April 2018 funding round that valued MD at $27.82 billion or RMB 189.47 B. Given that this is the private market value of the Company, incoming investors need to pay a premium in order to acquire the shares since after the IPO, MD shareholders will not be constrained from liquidating holdings if required. Rather than presenting our own estimate of a liquidity discount we use the Company’s internal assumptions as outlined in Figure 3 to arrive at more accurate equity value.

Figure 3: Assumptions used in valuing convertible redeemable preferred shares

Source: Accountant’s Report

With the passage of time and a maturing of the enterprise, the business of MD has become less risky. Disclosures outlined by the Company suggest an approximate 32% reduction in the liquidity premium from 19% in 2015 to 13% in 2017. With additional capital injection in April 2018, one can safely assume that the enterprise has been significantly de-risked already. Nonetheless, applying the 13% liquidity preference premium to the US$27.82 billion equity value, it appears that MD should be valued at US$31.9 billion.

How Much would be MD worth in April 2018 as a Public Company?

While that question is rhetorical, the point we raise is that when a business is fair-valued, which it was in April 2018, then what is it worth four months down the road in August 2018. Is it merely a question of the time value of money? We believe not.

After the successful IPO, the number of shares – prior to any allocation to IPO investors – will increase to 5.6735 billion, an increase of 8.7% from December 31, 2017, due to the vesting of RSUs and Stock Options. Therefore, in our view, MD is already valued at approximately $33.6B, or US$5.93/share. Our estimate excludes the 208.69 million shares that could vest under existing ESOP and executive compensation plans that will either vest or is granted after 2017.

Peak Valuation Maybe 40% higher Ignoring Competitive Intensity in China

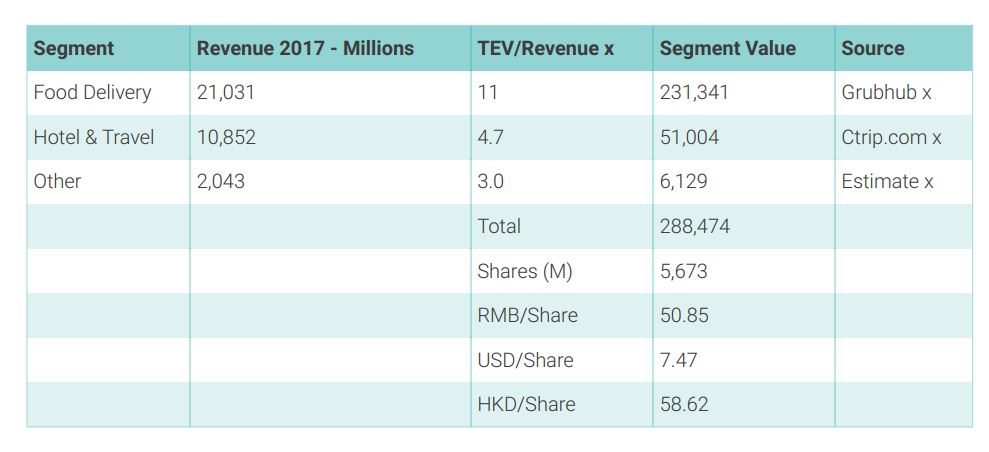

Many of our colleagues on the platform have dissected the financials and provided an opinion on margins, marketing dollars, business model etc. We give a frame of reference on the valuation that includes Grubhub Inc (GRUB US) (a somewhat similar publicly traded business in the U.S.) and Ctrip.Com International (Adr) (CTRP US) which is MD’s competitor in China.

Our benchmark involves a multiple on trailing revenue because MD’s EBITDA is negative.

Figure 4: Illustrative Equity Value

Source: ANTYA

GrubHub provides food delivery and ordering service in the United States and is currently trading at 11x 2017 trailing revenues. Similarly, Ctrip.com is trading at 4.7x. We believe Ctrip multiple is appropriate given the similarities between MD and Ctrip from a geographic, demographic and income standpoint. GrubHub, on the other hand, enjoys gross margins of more than 50%, compared to 8% for MD in the food service and delivery segment. Nonetheless, taking the data at face value suggests that upside to HKD 60/share or US$ 7.5/share is entirely plausible. We’ll have more to say on the economics and competitive intensity of MD’s food delivery segment later.

Investors subscribing to the IPO need to assess the how far below US$ 7.50/ share do they need to be to meet their return on investment threshold, and what discount to give from peak value on account of competition in China and dilution from IPO subscribers.