We believe Baidu Inc (ADR) (BIDU US) has taken multiple steps to de-risk its business by divesting the financial services segment, and via a successful IPO of iQIYI Inc (IQ US). Given the valuations of iQIYI Inc (IQ US) and Ctrip.com International (ADR) (CTRP US), we believe Baidu’s core search business is undervalued.

A rapidly growing Chinese economy and the wholehearted embrace of technology by its citizens has created unfathomable wealth and opportunities for early entrants into China. For the Tencent Holdings Ltd (700 HK), Alibaba Group Holding Ltd (BABA US) and Baidu Inc (ADR) (BIDU US) (“Baidu” or the “Company”) troika, China’s Internet economy is a gift that keeps on giving. At a rumoured $150 billion valuation for Alipay – a spin-off from Alibaba – it is already worth more than some of the largest, most successful and revered financial institutions of the world.

Motivated by the success that Alipay has had, many in China have entered the debilitating world of online micro-lending, hurting balance sheets, reputations and valuations. The list includes already public companies such as Qudian Inc (QD US), as well as in-house micro-lending operations at Baidu and Xiaomi. Importantly, Baidu seems to have realised the folly of online lending and has restructured its operations by divesting its financial services business as outlined in a press release dated April 29.2018, Baidu Enters into Definitive Agreements to Divest its Financial Services Business. The company will retain a stake of 42% in the business going forward allowing equity accounting instead of full consolidation, thereby relieving the stress of credit delinquencies and any loans and borrowings associated with funding the financial services operations.

The other business incubated by Baidu is the online streaming company iQIYI Inc (IQ US) or IQ. Given that China has other streaming players including Tencent’s streaming platform, some observers on Smartkarma

have been less sanguine about the prospects for IQ as discussed in IQIYI IPO Valuation: Throwing Good Money After Bad and IQIYI IPO: Tencent Video’s Metrics Point to a Stronger Business. The stock, however, has been on an exponential ride up and has risen 238% from the IPO price of $18/ADS on March 29, 2018, described in Baidu Announces Pricing of Initial Public Offering of iQIYI, Inc.

Given the plethora of initiatives in China to deepen financial markets, and increase domestic institutional and individual participation, including the introduction of CDRs discussed extensively in CDR Pilot Program – New Rules & 6?? Funds – It’s All Happening , at this moment an international institutional investor cannot be too sure of any scientific basis for equity prices of companies that might issue CDRs. Frenzied buying of CDRs by domestic retail and institutional investors, looking to partake in better-managed companies with more dependable disclosures, could cause equity prices to disconnect from fundamentals for an appreciable yet inestimable length of time.

Before this expected frenzy, Baidu appears favourable, especially given the discounted valuation accorded its core search business compared to its global counterpart, Alphabet Inc Cl C (GOOG US).

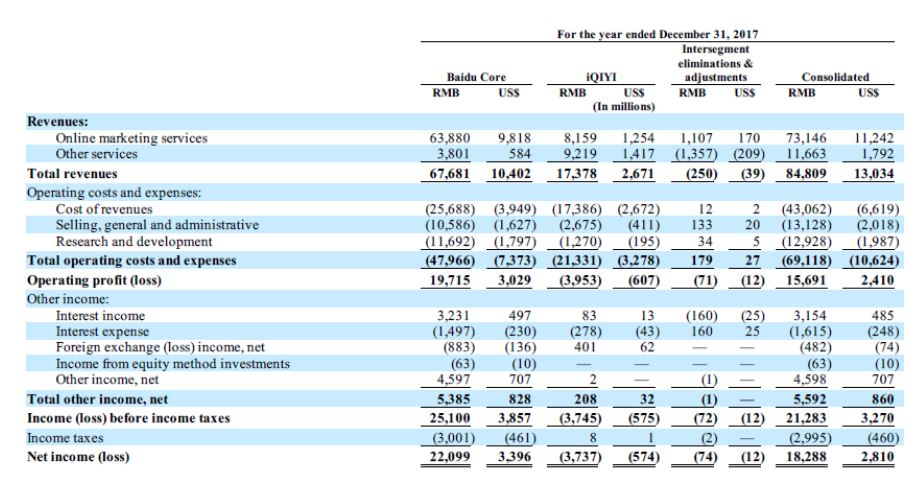

Figure 1 highlights the segment impact of IQIYI on Baidu’s core search business.

Source: Baidu Inc. 20-F & ANTYA

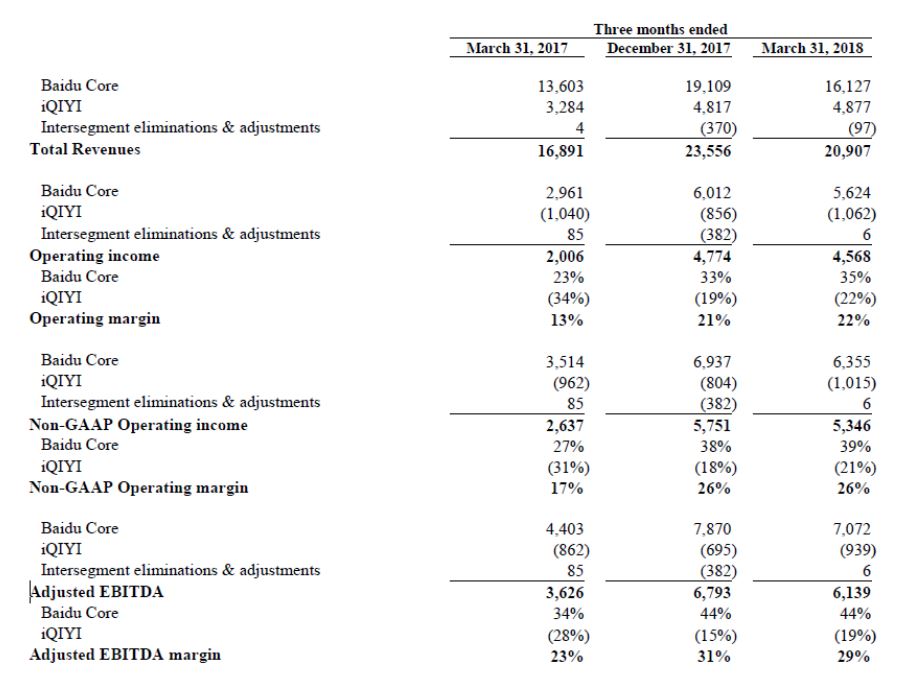

For 2017, Baidu’s core search business was burdened with $3.2 billion of incremental operating expense, while gaining only $2.6 billion of revenue, causing consolidating operating income dilution of $600 million, and operating margin reduction of approximately 11%. Baidu reported first-quarter results on April 26, 2018, and highlighted the disconnect and dilution caused by IQ consolidation on its financials and margins as illustrated in Figure 2.

Baidu Segment Margins – Better Times Ahead

Source: Q1-2018 Baidu Press Release and ANTYA

As highlighted above, Baidu’s core EBITDA grew 60% year-on-year, while EBITDA margins increased 10% to 44%. At the same time, IQ’s EBITDA improved from a negative 28% in Q1-2017 to negative 19% in Q1-2018. That brings us to the current valuation placed by investors on iQIYI and its impact on Baidu.

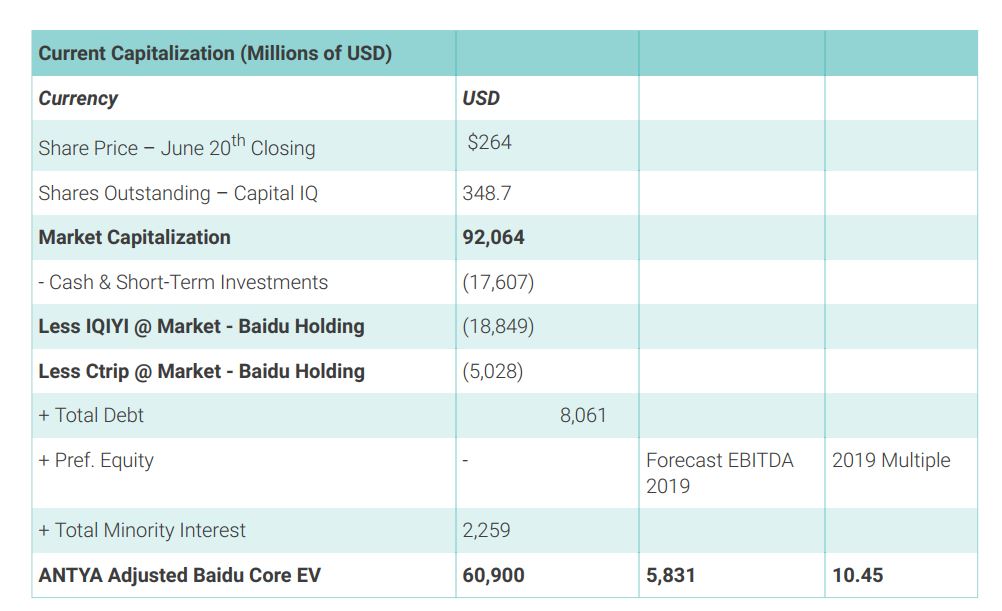

Figure 3 highlights core search is undervalued.

Source: ANTYA and Capital IQ. Numbers are rounded.

At its June 20, 2018 closing price of $264 Baidu’s market capitalisation is $92 billion. We deduct $17.6 billion of cash and equivalents as of April 26, 2018, and the current market price of Baidu’s holdings in IQ and in Ctrip.com of $18.8 billion and $5.2 billion respectively. We adjust for $8 billion of debt, to arrive at Baidu core enterprise value of $60.9 billion.

For 2017, Baidu reported segment operating margin of $3.20 billion as highlighted in Figure 1. We add $521 million of share-based compensation and $499 million of depreciation and amortisation to arrive at a $4.04 billion in EBITDA for 2017. With Baidu’s core search expected to grow at a compounded 20%, ANTYA’s 2019 search EBITDA forecast is $5.83 billion, implying a current core search EV/EBITDA multiple of 10.4x 2019 estimated EBITDA.

Alphabet is currently trading at 11.9x 2019 estimated consensus EBITDA. Both Baidu and Alphabet have multiple bets on self-driving cars, in AI, and in the cloud. Even if we were to apply a 20% discount to Baidu’s holdings in IQ and Ctrip, the company’s prospective EV/EBITDA multiple increases to approximately 11.0x, a 10% discount to Alphabet.

Moreover, if Netflix is an indicator of what could be in store for iQ, then based on a multiple of 7.59x 2020 estimated revenue of $6.3 billion, IQ could approach valuation of $48 billion, compared to $27 billion currently. Thus we believe that at the current levels Baidu is a safer and less volatile way to play the growth of streaming and proprietary content in China.