While active equity or bond management doesn’t stand discredited, enough academic and rigorously research quantitative evidence exists, that asset allocation and low-costs are much more favourable for the small investor. Although active stock picking is definitely a placeholder for great conversation, and may have a place in a diversified and much bigger portfolio (portfolios greater than $1 Million) most investors are well served with ANTYA’s low cost Astute Asset Allocation algorithm.

Ceteris Paribus ANTYA’s low fees can add 25% to your wealth over the longer term. These are after tax dollars that will Empower You.

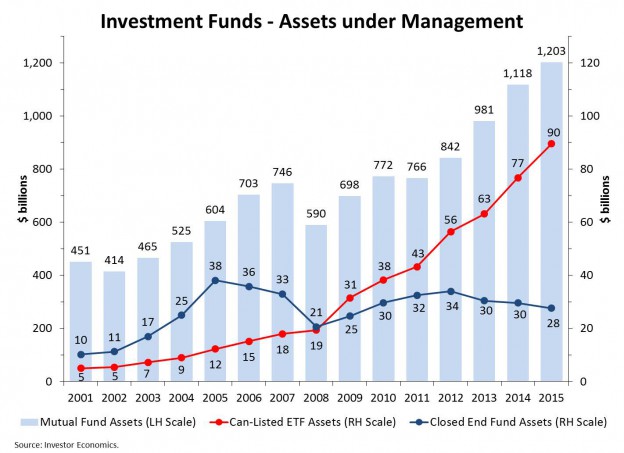

In the February issue of VITRAKA – citing research from an academic study – we highlighted that active mutual fund managers in Canada were “less active” than universally believed. Using data from the study, we illustrated that Closet Indexing in Canada was double that in the U.S., and that Canadians were paying higher fees than consumers in the U.S. (Canadians Paying for Underperformance) We called it a double whammy. It seems OSC is now interested in investigating the matter (we are not taking credit for it since the research has been out there for more than an year and newspaper outlets reported on the topic in 2015), and in its 2015 Summary Report on Investment Funds and Structured Product Issuers, the commission disclosed the following, and we quote:

“We commenced a targeted review of conventional mutual funds that disclose in their prospectus and marketing materials that they pursue active management strategies. Our review examined whether the funds are actively managed or whether they exhibit a close tracking of their benchmark index (often referred to as “closet indexation”).

Among other data, we considered the funds’ active share (a measure of the percentage of a fund’s portfolio holdings that differs from the composition of its benchmark index) to assess the extent of active management.

We have written to selected managers of Canadian equity funds to obtain a better understanding of their investment strategies and the reasons why the strategies resulted in investment portfolios that overlap significantly with the composition of their benchmark index. We have received responses and are in the process of reviewing and requesting additional information, including whether the securities selection process for the funds is affected by the managers’ evaluation of their funds’ performance relative to their benchmark index.”

ANTYA believes that this topic is of more than an academic interest to the regulators. Given the various steps taken by regulators over the years to bring transparency to fees, it is extremely important for the Commission to make an independent and robust assessment of mutual fund performance and fees. Most importantly, in a low return-high volatility environment, if regulators can ensure that clients get what they pay for, all stakeholders will feel justified in their position.

Nonetheless, while active equity or bond management doesn’t stand discredited, enough academic and rigorously research quantitative evidence exists, that asset allocation and low-costs are much more favourable for investors than anything else. While active stock picking is definitely a placeholder for great conversation, and may have a place in a diversified and much bigger portfolio (say a portfolio greater than $1 Million) most investors are well served with ANTYA’s low cost Astute Asset Allocation algorithm.

Ceteris Paribus ANTYA’s low fees can add 25% to your wealth over the longer term. These are after tax dollars that will Empower You.